Make sure you purchase an owner’s title insurance policy to protect your property rights. Find out how for a one-time fee an owner’s policy can protect your important property rights for as long as you or your heirs own the property. Also, learn about common and real-life title problems that could impact your property rights.

Get an Owner’s Policy to Protect Your Property Rights

Lenders require a title insurance policy to protect their investment. You should have a policy to protect your investment as well. For a one-time fee paid at closing, an owner’s policy can protect your property rights for as long as you or your heirs own the property.

An owner’s policy protects you from:

- Unpaid mortgages

- Unpaid property taxes

- Child support liens

- Missing heirs who could claim the property belongs to him or her

- Missed easements or rights of way that could limit your use of the property

There are two types of title insurance policies. As mentioned, the owner’s policy protects the homebuyer. A loan policy protects the lender. This policy also benefits the borrower because it provides an initial source of coverage and compensation in the event of a challenge to the borrower’s title or lender’s lien priority. Most lenders usually require a loan policy when they issue you a loan. The loan policy is based usually on the dollar amount of your loan. It only protects the lender’s interests in the property should a problem with the title arise. It does not protect the buyer. The policy amount decreases each year and eventually disappears as the loan is paid off. An owner’s policy, usually issued in the amount of the real estate purchase, provides protection for as long as you or your heirs have an interest in the property.

Real-life Title Problems

Missouri Couple Saved from Foreclosure

A couple purchased a home from their landlord, who had taken out a $419,000 loan to purchase the property along with several other properties. The lien was missed during the title search, so the lender paid the landlord instead of paying off the lien. Despite making their payments, the bank sent a letter saying the home would be auctioned. Because the couple purchased an Owner’s Title Insurance Policy, the title company paid the lien and the husband and wife kept their home.

Texas Builder Sells Homes With Liens

A Texas-based builder sold first-time homebuyers houses that were encumbered by undisclosed liens. When Casa Linda Homes subsequently failed to pay its undisclosed debt, the creditors who were owed money then instituted foreclosure proceedings or filed lawsuits against the homebuyers. Because the deals were “seller financed,” the builder didn’t require the buyers to purchase title insurance, which would have protected the buyers.

Vacant Virginia Properties Fraudulently Sold

In Virginia, properties were sold to unsuspecting buyers. Unfortunately, the sellers weren’t the rightful owners of the properties. Instead, death certificates of the real owners were falsified and the fraudsters appeared at settlement to sign the closing documents. The criminals were caught and the properties were returned to the rightful owners. But what about the unsuspecting buyers? If they had purchased an Owner’s Title Insurance Policy they would have been covered. However, if they weren’t properly advised to protect their investment they would not have only been without a home, but also lost their entire down payment.

Calif. Non-profit Dissolves After Losing Suit

Mendocino Coast Television voted to dissolve its non-profit organization after losing a lawsuit that found the TV station never really owned its headquarters. An Owner’s Title Insurance Policy would have covered the costs of the non-profit’s lawsuit.

Underground Utility Lines

After a months-long search, you finally find your family’s dream home—a safe neighborhood and great schools, and a big backyard for the swimming pool you plan to build. You move in and hire a contractor, but a few days into construction the contractor finds an underground utility line running right through the middle of your backyard. You check your owner’s policy and find out that the title search did not discover this easement.

If the homeowner purchased an owner’s policy, their title insurance company would pay to have the underground utility relocated so they could build their swimming pool.

Fraud and Forgery

Fraud and forgery are examples of hidden title hazards that can remain undetected until after a closing despite the most careful precautions. Although emphasizing risk elimination, an owner’s policy protects you financially through negotiation by the insurer with third-parties, payment for defending against an attack on the title as insured, and payment of valid claims.

Innocent buyers purchased a home site through a real estate company, accepting a notarized deed from the seller. After the purchase, another couple—the true owners of the property who lived in another city—initiated legal action to prove they actually owned the property. Because the innocent buyer purchased an owner’s policy for a one-time fee at closing, the title company provided a money settlement to protect against financial loss.

As it turned out, a forger spent time in advance at the local courthouse, searching the public records to locate property with out-of-town owners who had been in possession for an extended period of time. The individual involved then forged and recorded a deed to a fictitious person and assumed the identity of that person before listing the property for sale to an innocent purchaser, handling most contacts through an answering service. Also, the identity of the notary appearing on deeds was fictitious as well.

Homeowners without this coverage would have lost their home.

REMINDER: For a one-time fee, an owner’s policy provides protection for as long as you or your heirs on the property. In addition to protecting your investment, an owner’s policy also covers the legal fees and the cost of defending your property rights.Parts of a Title Policy

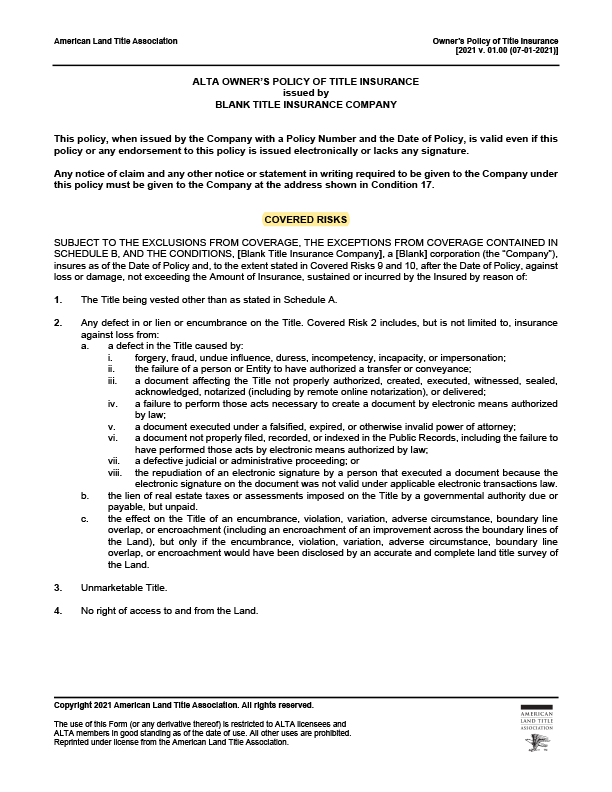

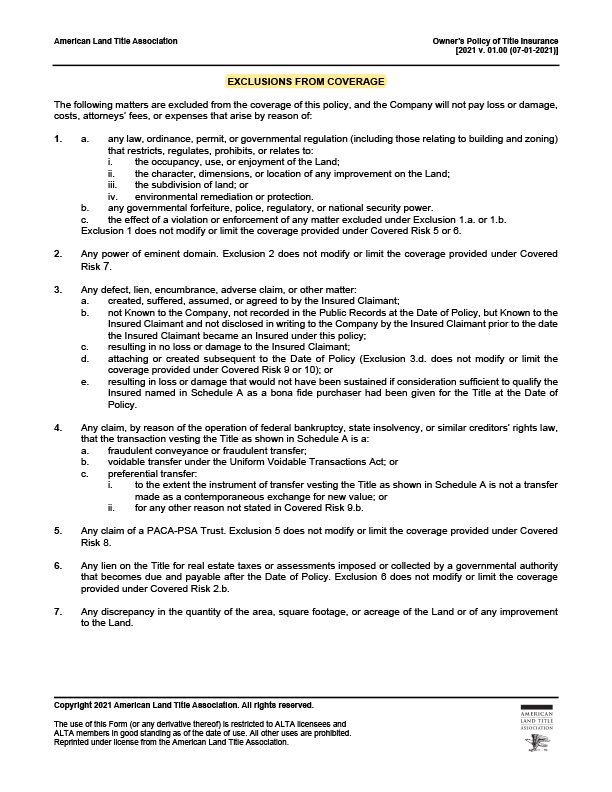

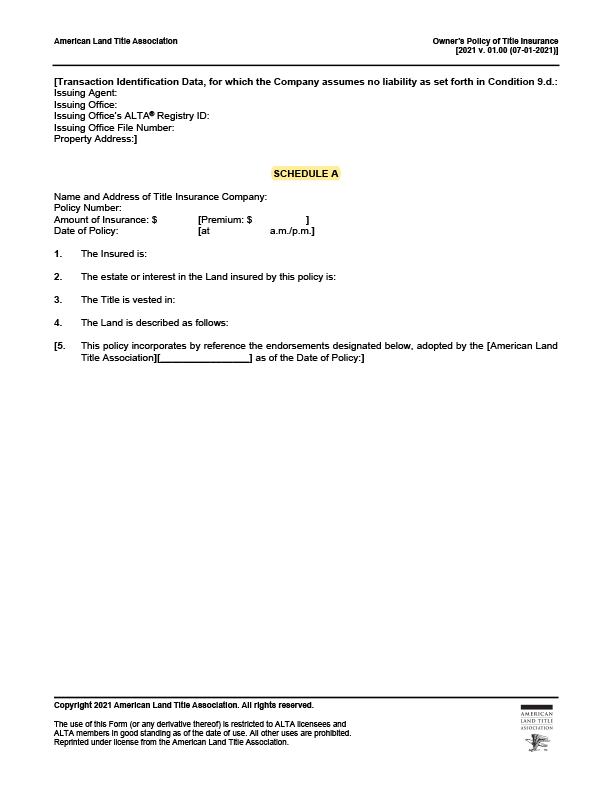

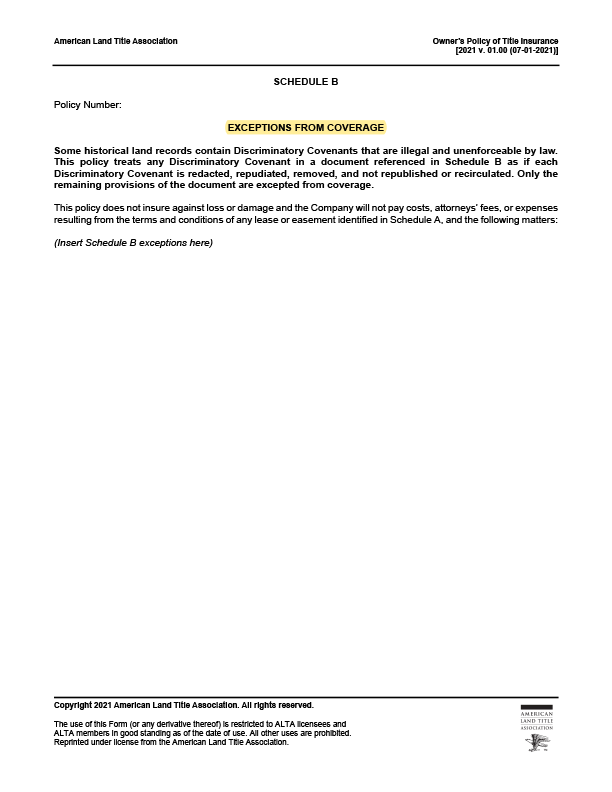

The owner’s policy has five sections: covered risks, the exclusions from coverage, Schedule A, Schedule B and the conditions. Click here for a pdf.

1. Covered Risks

This section lists what kinds of risks the policy insures against. However, the policy makes it clear that the insurance of the listed risks are subject to (1) the Exclusions listed following the Covered Risks, (2) any exceptions listed in Schedule B, and (3) the Conditions. In the most current ALTA Owner’s policy, there are ten covered risks listed in the policy. Some of the most important covered risks are:

- the risk that someone else owns your property

- that there is some defect or encumbrance on your title caused by fraud or forgery

- any liens for real estate taxes or assessments that are due but unpaid

- that your title is unmarketable, that is, you are unable to sell your property to a purchaser because of a title defect

- right of access to and from your land.

Review your owner’s policy or ask your title agent about the covered risks included in your policy.

2. Exclusions

Exclusions limit the coverage of the policy. They deal with issues that are outside the control of the title company. The ALTA owner’s policy contains five exclusions, which include matters such as governmental regulations on the land and eminent domain, as well as title matters created or agreed to by the insured, or title defects known to the insured but not disclosed in writing to the title company prior to the date of the policy. The policy does not insure against any defect or title issue that is created or attaches to the property after the date of the policy. Also, the policy does not insure against the effects of bankruptcy law on the transaction creating the insured interest.

3. Schedule A

Schedule A sets forth the specific information on the title and policy, such as the date of policy, the amount of insurance, the insured, the legal description of the land insured by the policy and the estate insured, such as fee simple or leasehold. Schedule A must be attached to the policy in order for the policy to be valid.

4. Schedule B

Schedule B lists the various exceptions to the title that the title company found when it performed its title search. Common exceptions would be things such as prior unreleased mortgages on the property, easements, taxes, restrictions on the use of the property, and any other limitations on the title such as homestead rights or survey issues if no survey has been performed. By listing various items as exceptions, the title company is telling the insured that these items are not covered by the title policy, and that the title company will not pay a claim or defend against a claim based on these excepted items.

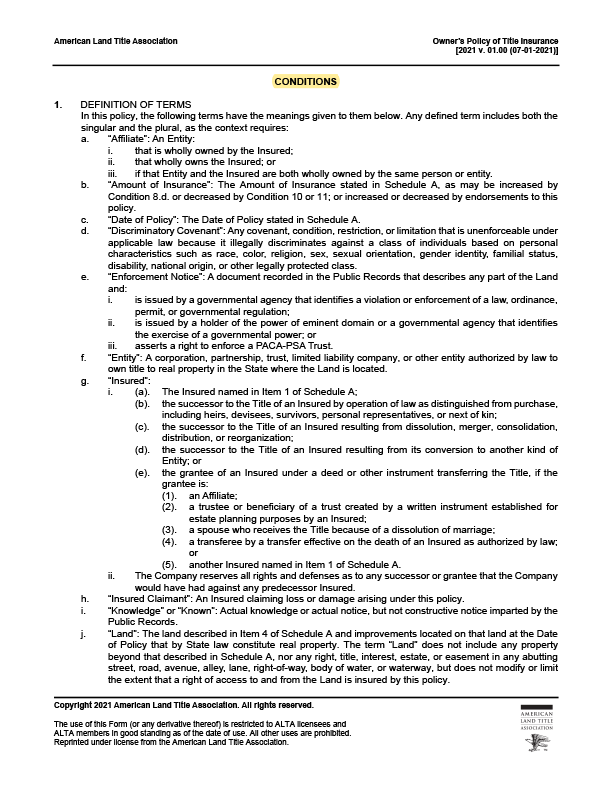

5. Conditions

This section outlines the relationship between the insured and the title company. Paragraph 1 contains the definitions of certain terms used in the policy. Terms such as “Insured,” “Insured Claimant,” “Knowledge” and “Public Records” are defined so as to eliminate any ambiguity. There are several different paragraphs setting out how a claim under the policy is handled, including how to provide notice of a claim, what is required to prove loss, and the requirement that the insured must cooperate with the title company in the handling of the claim. Click here to learn how to file a claim. The Conditions describe the rights of the title company to pay or settle the claim, and the determination, extent and limitation of liability. Most policies also contain a paragraph that allows the insured or the title company to demand arbitration if the amount is under $2 million.

Cost of Title Insurance

The cost of a title insurance policy relative to the cost of a property transaction is about one-half to one percent of the purchase price. The premium is based on the purchase price of the property, generally determined by the value of the land plus any improvements.

Who Pays

Title insurance industry practices vary due to differences in state laws and local real estate customs. Who pays for the owner’s policy varies from state to state. On the East Coast, the buyer typically pays. The seller normally pays on the West Coast. A discount may be available when both the owner’s and loan policy are purchased simultaneously. Ask your title company who pays in your area and if a discount is available.

It’s also important to note that the cost for title insurance may include other services provided by the title company such as the title search or conducting the closing. When comparing one rate to another, be sure to get detailed information on what is included in that rate, so you are comparing equally.

Regulation

Title insurance rates and products are regulated by state insurance departments. In addition, title insurance and real estate closing practices are regulated by the Consumer Financial Protection Bureau (CFPB).

In most states, title insurers are required to file their rates prior to usage, with regulators either reviewing those rates before or shortly after they go into use.

State regulators in some states, including Florida, New Mexico and Texas, set mandatory statewide premiums.

Shop Around

There are many factors to consider when selecting a title insurance company, such as local expertise, service standards, market conduct and commitment to the community. Be sure to shop around and ask questions to make sure you’re comfortable with your title company and that you know what’s included in the cost.

Many consumers rely on their real estate agent or mortgage lender for a recommendation for a title company, however, it important that all homebuyers remember that they have the right to shop for title insurance and to choose their own title agent or company.

How to File a Claim

An owner’s policy of title insurance provides the homeowner peace of mind about their legal rights to real property.

If you have a question or concern about your rights, promptly notify the title insurance company whose name appears on the title policy. The title policy includes instructions for contacting the title insurer. This information is usually at the end of the “Conditions and Stipulations” section within the policy.

Unable to locate your policy or unsure whether you purchased a policy? Contact the title company, title agent, settlement agent or attorney that handled your purchase and inquire about your coverage.

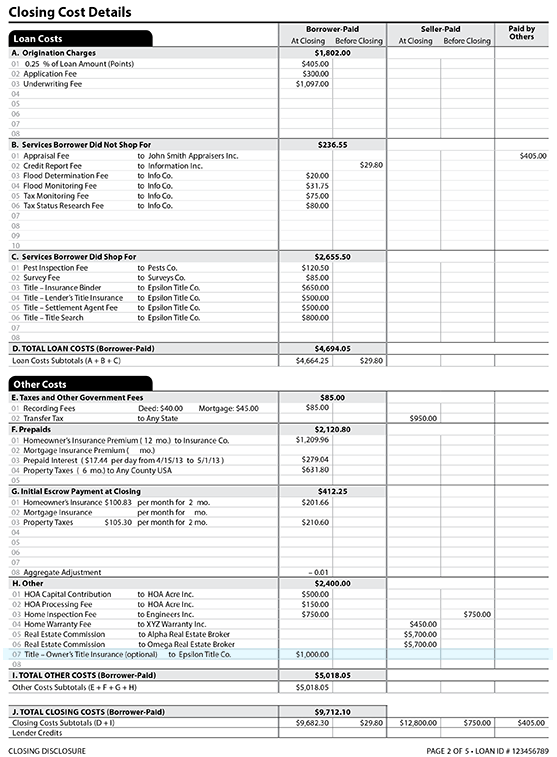

You can determine if you have title insurance coverage by reviewing the Closing Disclosure provided at the closing of your purchase. For example, charges for an owner’s policy can be found under the “Other Costs” section on page two of the Closing Disclosure.

{kind=link}

Contact information for the title insurer may also be found online or with your state department of insurance.

When giving notice of a potential claim to the title insurer, include the property address, a brief statement of the question or matter, copies of any claims documents received, and a copy of your owner’s policy (if available).

Remember, the broad coverage of title insurance includes protection against frivolous claims, or title issues that may not present an immediate problem. It’s best to contact the title insurer promptly, as soon as you have any question or concern about your legal rights with insured land.

Title Search

A professional will search public records for debts, legal judgments and other homeownership issues to give you peace of mind in your investment.

Some of the items reviewed include:

- prior deeds

- mortgages

- divorce decrees

- court judgments

- delinquent taxes

- child support payments

A title professional will also look for covenants, conditions and restrictions and other types of easements. When an issue is discovered, the title professional will take care of it—typically without you even knowing about it. If the problem is not easily resolved, you will be notified. Title searches reveal problems on more than a third of all residential real estate transactions.

Unknown Issues

Some title issues are not apparent from a review of the public record. Title insurance provides coverage for undisclosed title defects that might later result in a claim.

Unknown events include:

- forgery

- documents signed by minors or someone incompetent

- deeds executed under an expired power of attorney

- errors on the public record

This work is necessary to issue the insurance policy and often includes the cost of conducting a title search, examination, correcting errors, issuing the policy, and, frequently, the settlement or closing for consumers.

An owner’s policy protects against these additional items.